4 key takeaways from PGC Barcelona: D2C’s reality, star names flock to Spain, and going AI-first

This week we hosted Pocket Gamer Connects Barcelona for the second year running - and it was another big success.

The event had more than 1,100 registrations across all activities, while over 1,600 meetings were arranged through our online networking platform.

We had speakers from the likes of Tetris, FunPlus, Scopely, Zynga, Gameloft, Ubisoft, Wooga, Digital Legends and many more.

So what were the big takeaways from the show? Below we’ve rounded up a few of the highlights and talking points.

-

The direct-to-consumer reality

I hosted a talk on D2C sales, delving into how much revenue publishers are actually making from their direct-to-consumer strategies. The verdict? Well, from the perspective of D2C share, some top publishers have shifted significant sums to their own platforms.

As I noted in this article, which the talk was based on:

- D2C accounted for 39.2% of Playtika’s sales in Q1. The publisher said its annual run-rate has neared $1.2 billion.

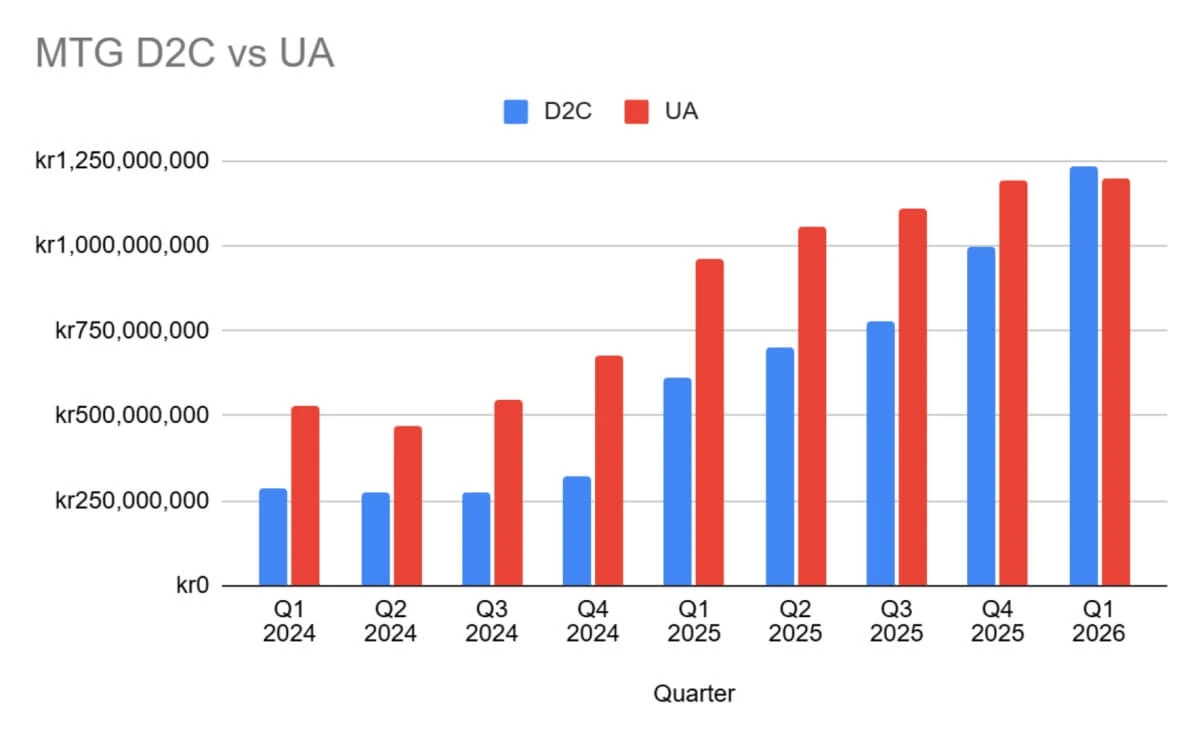

- Modern Times Group said D2C made up 39% of group revenue in Q1 2026.

- Stillfront Group reported that 44% of bookings are now going through the publisher's D2C platform.

One question that arises from shifting revenue to D2C and away from platform fees is: where does that money go? One interesting chart looking at MTG's D2C sales versus user acquisition investment showed both rising in step with each other:

I asked ByteBrew chief strategy officer Christopher Lefebvre about rising UA costs and he commented:

“UA demand doesn't really bend. Studios need installs to survive, so they keep buying even as it gets more expensive, and the platforms have no reason to ease off. Put that on a payback window that now runs months, sometimes years, and it stops being about any single auction. It's just the shape of the market.”

Elsewhere, I hosted a couple of panels on the world of D2C. On one of those, I asked what is a realistic share for studios to target when shifting revenue to their own platforms.

Worldline director of channel sales Jonas Martins said while there are companies pushing for 50%, most smaller studios should be aiming at 15% to 20% and building from that. Xsolla business development manager - EMEA Inês Ramalho put the floor a little lower for the smallest teams, at around 10% to 15%, with more established studios able to push higher.

I asked the same panel what they thought of that Google and Epic deal that set a 20% store fee for the Play Store, among other changes. They expressed disappointment over the agreement, still pending approval in the US from the judge in the case.

-

International companies have flocked to the region

Spain has become a major European games hub. The companies that have set up in the region, a number of which we named in our Top 30 Iberia Game Makers list, reads like a who’s who of the global games industry.

There are companies such as Scopely, Paradox Interactive, Ubisoft, King, Zynga, FunPlus, Gameloft, IO Interactive, Larian Studios, Outfit7 and Tripledot Studios. Meanwhile, over in Portugal, Miniclip has a major studio, with Funcom also setting up a base in Lisbon through the acquisition of work-for-hire studio Zona Paradoxal (ZPX).

Then there are the home grown studios like Socialpoint, Lingokids (which recently raised $120 million), Digital Legends, Nomada Studio, Axes in Motion, Bluetile and others.

The growth has come over time, boosted by companies like Gameloft, which has operated in the country since 2000. Then there are the aforementioned successes of Socialpoint and Digital Legends, with the former acquired by Take-Two and the latter by Activision, throwing other big names into the pool.

Meanwhile, Scopely’s Co-CEO Javier Ferreira, a Spanish native who saw the opportunities in Spain, has seen his company invest significant in the country. The publisher has acquired local studios like Genjoy and Omnidrone and set up a major base that employs more than 1,100 staff across the region. The teams played a key role in the development of global blockbuster Monopoly Go.

The big challenge for Spain now is building new homegrown IP that scales internationally, competing with the world’s top games. As Side Quest Games co-founder Alexandre Besenval told us:

“Although the Spanish ecosystem is incredibly dynamic, and has already produced a lot of strong companies and IPs, it has not yet reached its ‘final form’: the creation of a local, homegrown unicorn company or game, akin to successes seen in Sweden (King), Finland (Supercell, Rovio), Turkey (Dream Games), or France (Voodoo).

“Achieving this milestone would be transformative for the country. It would significantly attract more talent and investment, and it would spur the creation of spin-off studios enriched with high capital and expertise (the “ex-XX mafia” effect).”

-

The AI impact

Inside the games industry, it seems as though the debate over whether to use AI is fading - though not gone completely in the West - and has moved to how new technology can be harnessed practically for production and marketing.

I spoke with FunPlus chief business officer Chris Petrovic on stage covering a range of topics, largely centered around building new companies and getting investment. Asked if having AI in your deck to get investment is necessary in the current market, Petrovic succinctly put: "If you're not doing it, your competitors will be."

For FunPlus itself, which operates games including State of Survival, King of Avalon and is set to publish Animo, the “goal is to be an AI-native games company”, said Petrovic. That tracks with other major publishers that are being public about their ambitions - including Krafton’s bid to invest $69m to become an AI-first company and HoYoverse’s reported $14.7bn investment in the tech. Other publishers are investing at varying degrees, but aren’t so open about it.

FunPlus is currently in an “advanced discovery phase” with AI, part of an “experiment, then standardise” model. It’s giving teams agency to experiment with tools - within financial reason - before those learnings can be potentially adapted into a standardised approach for the business.

Some concerns linger for AI adoption, even by those that are excited by the possibilities. One attendee questioned what new genAI tools mean for junior developers if certain coding jobs are taken over by tech.

Typically, he said, junior developers would be given tasks to learn their trade. So how will their training and development look in the future? It’s another practical challenge that studios will have to adapt to.

-

Is there more money than ever available in games?

The games industry’s investment challenges are no secret - it’s tough out there to get funding or cut a deal with publishers.

But one speaker and investor cut a more positive tone at PGC Barcelona. GameFounders co-founder Kadri Harma claimed during a panel that “we are at the point in history when there is the most money ever available for games”.

She pointed to funding support provided by various regions and countries, including grants by the European Commission and government support in countries like Canada, Turkey, France, UK Finland, with some countries also expanding these schemes.

“You have VCs that are raising hundreds of millions. You have publishers, you have UA funding. Griffin just announced a $100m rev share fund. Never in the history of life on this planet has there been more money available for games. So I’m not going to agree to there not being money.”

Harma did note a challenge for VCs, with some portfolios full of games they can’t get their money out of because there are no buyers - a consequence of industry consolidation.

Looking to the future, Harma believes the industry is set for another big shift, akin to the West’s move to free-to-play back in 2012. With the dismantling of the app store duopoly, the onset of AI and other industry challenges, “money is going to find different ways to flow”.

Kokoon Games CEO Henri Lindgren, also on the panel, agreed with Harma’s points. He added, though, that investment has moved from a merit-based system to a metric-based one in which studios have to prove themselves.