H1 2026 genre analysis: strategy stumbles, RPGs fall, and puzzle revenue ramps up

| Date | Type | Companies Involved | Key Datapoint |

|---|---|---|---|

| Jul 16, 2026 | report | AppMagic Century Games Dream Games First Fun HoYoverse King Microfun Mixi Nexon Peak Games Playrix Roblox Tencent The Pokemon Company | $40 billion |

- Strategy stayed on top as the highest earner, making $9.1 billion this H1.

- This marked a 4% decline year-over-year.

- RPGs saw a sharper fall of 14%, down from first to third place over two years.

- The puzzle genre accelerated with 20% global growth, reaching second place.

Mobile games generated a collective $40 billion in gross player spending between Google Play and the App Store during the first six months of 2026, a marginal decline of less than 1% year-over-year.

Strategy stayed on top as the most lucrative genre of the period after dethroning RPGs in 2025.

During H1 2026, AppMagic estimates suggest the strategy genre generated over $9.1bn in gross player spending, specifically between Google Play and the App Store. True earnings were likely even higher when considering revenue from alternative stores and increasingly prevalent web shops.

Focusing on the major stores, strategy represented 23% of all player spending on mobile this past half year. However, its top position came despite falling revenue, down 4% Y/Y from $9.5bn in H1 2025 - when the genre was recording the third-highest growth of any on the platform.

However, strategy is far from the only genre seeing some decline, with six others falling while nine grew Y/Y.

Strategy’s fall in revenue was also far less stark than the RPG genre’s decline, continuing to lose its momentum. This H1, RPGs lost the silver medal for total revenue to the puzzle genre with a fall of 14% Y/Y. From almost $8.2bn in the first half of 2025, RPGs collectively made just $7bn in H1 2026.

Puzzle games, meanwhile, picked up $7.6bn this H1 with the second-strongest growth rate on the global market, up 20% Y/Y. This made puzzlers one of just three genres to rise up the rankings during the period, meanwhile kids’ games overtook AR and party games overtook the racing genre.

The success of the puzzle genre was largely due to the US, accounting for 48% of its global revenue.

The strongest in strategy

Strategy’s dominance this H1 was led first and foremost by Tencent’s Honor of Kings, which maintained its position as the highest-grossing game in the genre and on mobile at large during the period. In fact, Honor of Kings was the top-grossing mobile game every single month in H1.

It’s generated almost $1.3bn between the major app stores during the timeframe, accounting for 14% of the entire genre’s global revenue.

Century Games’ Whiteout Survival followed as the second most impactful strategy game, having generated $944.8m for the genre over the first half of the year. It’s overtaken FirstFun’s Last War: Survival in the process, now rounding out the top three with its $932.1m.

These top three strategy games all saw slight declines in revenue compared to H1 2025, but even so, combined they generated over $4.5bn of the genre’s total $9.1bn, accounting for approximately half of all strategy’s earnings.

Pokémon TCG Pocket and Tencent’s Golden Spatula rounded out the top five.

Rambunctious RPGs

It was a similar story for RPGs, shrinking Y/Y with smaller contributions from many top performers. Last H1’s genre leader Honkai: Star Rail took a 35% hit with a fall from $301m to $196.1m, dropping from first place to fourth.

While this allowed Genshin Impact space to top the genre’s charts, continuing developer HoYoverse’s stay at the pinnacle of RPGs, Genshin also decreased in revenue slightly from $280m in H1 2025 to $257.9m in H1 2026.

The open-world gacha was followed closely in second place by Nexon’s MapleStory: Idle RPG, just $1.5m behind. The game exploded onto the scene in 2025 and has quickly shot to over $350m in lifetime revenue in less than a year.

Mixi’s Monster Strike ranked third in H1 2026, making $209m during the period.

These top three combined generated $723.2m in the first half of the year, equating to just over 10% of the RPG genre’s $7bn global revenue. They therefore represent a smaller share than strategy’s top three, suggesting more RPGs are seeing a fair share of their genre’s pie even if it’s a smaller meal overall.

In fact, top RPG Genshin Impact made just 20% of the earnings generated by strategy leader Honor of Kings.

Puzzle’s strong performance

Meanwhile, the puzzle genre came out of H1 as the real winner, one to watch with its upwards trend and momentum. While the broader mobile games industry shrank slightly this H1, puzzlers grew by 20% Y/Y from $6.3bn to $7.6bn.

This rate of growth was second only to party games, which achieved growth of almost 29% but ranked as a much smaller genre overall. Puzzle games, on the other hand, had already accelerated their genre into third place during H1 2025. Now, the genre ranks second.

It’s being led by Dream Games’ Royal Match, which generated $883.7m during the first half of this year. That’s a 12% share of the puzzle genre’s global player spending.

Microfun’s Gossip Harbor ranked second, overtaking 14-year-old puzzle veteran Candy Crush Saga and pushing the latter into third. This top three represents 32% of the genre’s earnings, accounting for a larger share than RPGs but still smaller than strategy’s top-three dominance.

Also in puzzlers, Playrix’s Gardenscapes fell into fifth as it was overtaken by 2024’s Royal Kingdom, another title seeing record growth this year. In fact, Royal Kingdom is already well on its way towards $1bn in lifetime earnings, with 42% of all its player spending generated this H1.

The top five looks slightly different in the US, with Royal Match still on top but Candy Crush in second. Gossip Harbor, Royal Kingdom and Peak Games’ Toon Blast filled out H1's top five.

US players spent more on puzzle games than any other genre this H1, at over $3.6m. That was almost four times as much spending as on RPGs and 54% more than on strategy games. In fact, this market spent more on mobile puzzle games than on RPGs and strategy games combined.

Around the globe and in the US

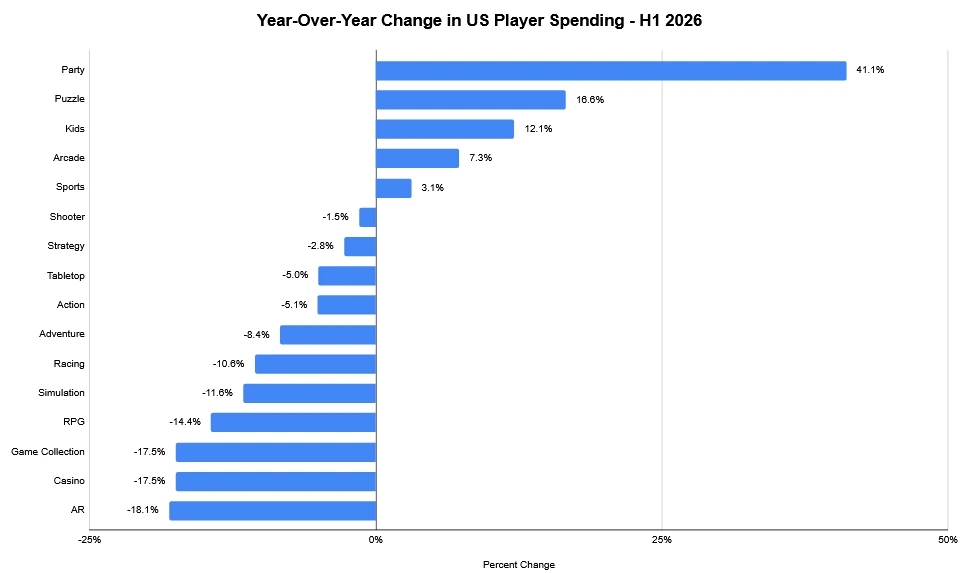

The US market accounted for 31% of worldwide player spending this H1.

Its biggest impacts were on puzzle, casino, kids and tabletop games, responsible for more than 40% of all spending in these categories. It’s little surprise, therefore, that they ranked higher on US revenue charts than on the global stage.

On the opposite end, the US gave the smallest contributions to party games, RPGs and shooters, at 13%, 14% and 15% respectively. RPGs actually ranked fifth overall in the country, with simulation games having more impact.

The highest-grossing simulation game was Roblox, making $806.9m on mobile worldwide. It was also on top of the genre in the US, responsible for $349.5m of that sum.

A total of five genres saw growth in the US - one fewer than did globally - with puzzle, party, kids and arcade games growing in both. Notably, while the US was a key player in puzzle’s success, its growth rate in the country was actually slightly lower than was observed globally.

Tabletop games saw a similar case, making the largest share of their earnings from the US but actually shrinking marginally in the country, meanwhile growing globally.

With just five genres growing in the States while 11 declined, overall mobile revenue from the market also fell from $12.6bn in H1 2025 to $12.2bn in H1 2026, a 3% drop. It’s a sharper fall than was seen globally, but last year player spending did pick up slightly in H2.

And, with some studios now reporting serious direct-to-consumer revenue - worth $17 billion today, or around 15% of the global in-app purchase sector - it’s entirely plausible that the slight fall in observed spending on major stores isn’t reflecting an actual decrease.

Rather, this may be the result of changing times and regulations, a shift in where players are spending, successfully converting to web shops for stronger deals, unique bundles and more.

Companies