The race to 2030: How MENA governments turned games into a national ambition

- Saudi Arabia is the only country in MENA where 2030 gaming targets are backed by capital already deployed, but the EWC relocation to Paris showed even the most funded vision is not insulated from regional volatility.

- Dubai is the outlier in this race, targeting 2033 rather than 2030, and is only now beginning the shift from attracting foreign studios to building its own.

- Morocco has the most ambitious targets relative to its current base, but the gap between ministerial vision and commerc

Across the Middle East and North Africa, governments are pinning their ambitions on becoming gaming powerhouses by 2030. Saudi Arabia, the UAE, Morocco and Egypt are all working towards that same deadline.

That is not a coincidence. It traces back to 2016 in Saudi Arabia when crown prince Mohammed bin Salman unveiled Vision 2030 as a blueprint to diversify the Kingdom away from its reliance on oil. Games would later emerge as one of the sectors expected to support that diversification.

At the time, the scale of Saudi Arabia's games ambitions was widely underestimated. A decade later, similar ambitions have emerged across the region, with neighbouring governments even adopting the same timeline.

Whether real plans back those ambitions - or whether 2030 is simply a number that sounds far enough away to be ambitious and close enough to be credible - is what this piece sets out to examine.

Saudi Arabia: the original blueprint

Saudi Arabia's National Gaming and Esports Strategy, launched in September 2022, remains the most ambitious and best-funded gaming vision in the MENA region.

Channelling more than $38 billion through the Public Investment Fund (PIF) and Savvy Games Group, it targets 39,000 sector jobs, 250 gaming companies, 30 globally recognised games and a $13.3bn contribution to GDP by 2030. No other government in the region has produced anything comparable in scale or institutional depth.

The money is not merely pledged - it is being deployed. In the most significant single transaction in games history, EA shareholders approved a $55bn acquisition led by PIF, which now owns 93.4% of the company, taking it private after more than 40 years. Savvy separately announced plans to acquire Moonton from ByteDance for $6bn.

Last year's Esports World Cup in Riyadh attracted around three million visitors and featured a record $70m prize pool, eclipsed only by this year's $75m edition. Meanwhile, Qiddiya, the PIF-backed entertainment city remains on track to deliver a dedicated games and esports district with four world-class arenas, including one of the largest esports stadiums.

Building a domestic industry

The investment ecosystem now extends beyond PIF. Impact46 has invested $53m in Kammelna and a further $6.7m across five Saudi game studios.

Merak Capital launched an $80m gaming fund in late 2024 alongside Exel by Merak, an accelerator backed by the National Development Fund. Exel invested $5.1m across 17 startups in its first cohort, each receiving $300,000 in equity funding, and has since become the first gaming accelerator to join the Riyadh Creative District.

The Saudi Game Champions Program launched its second edition in 2025, providing each selected startup with $53,000 plus mentorship from global industry figures. These are modest early-stage signals, but together they suggest a funding layer beyond sovereign wealth is being formed.

Ambition meets reality

However, the picture is not without complications.

PIF is reportedly facing constraints on fresh capital as substantial wealth remains tied up in illiquid megaprojects, including NEOM. That does not threaten commitments already made, but it raises questions about the pace of future investment.

Geopolitical risk has also become harder to ignore. The 2026 Esports World Cup was moved from Riyadh to Paris just eight weeks before it was due to begin after regional instability linked to the Iran conflict raised concerns over international travel and safety.

The Esports Foundation maintains that Riyadh remains the tournament's long-term home, but the relocation illustrates that Saudi Arabia's gaming ambitions are not immune to wider regional instability, as Savvy Games Group CEO Brian Ward has previously acknowledged.

Meanwhile, Sandsoft closed its Riyadh and Barcelona offices last year to focus on publishing, a reminder that even the most capitalised games nation in MENA is not shielded from the industry's broader structural and commercial pressures.

Racing towards 2030

Despite the challenges, Saudi Arabia remains the only country in MENA with a 2030 games strategy backed by substantial capital already deployed and institutions already in place.

The question is no longer whether the Kingdom will invest, but whether it can build sustainable domestic capability before the deadline arrives.

Savvy's recent partnership with Roblox signifies that urgency. The partnership aims to use Roblox's educational tools and Creator Hub to introduce more than 700,000 Saudi high school students to game development and strengthen the domestic talent pipeline.

However, Roblox remains a controversial partner, having been blocked in several countries over child safety concerns and facing multiple lawsuits in the United States. That Savvy proceeded regardless says something about the pressure to manufacture talent at scale before 2030 arrives.

UAE: Building the ecosystem

Dubai's formal gaming programme targets 2033, not 2030 - a distinction that sets it apart from every other country on this list. The Dubai Program for Gaming 2033 was launched in November 2023 and has since grown the city's games ecosystem to more than 350 companies, including 260 specialised game developers by mid-2025, with formal targets to create 30,000 new jobs and contribute $1bn to GDP by 2033.

There's also the case for emerging technologies. UAE authorities forecast that AR and VR will contribute $4.1bn to the national economy by 2030, creating 42,000 jobs and boosting GDP by 1%. The consumer base is engaged and willing to spend, which is why international studios are paying attention.

The Dubai Esports and Games Festival 2026, its largest edition yet, drew 43,000 attendees across 17 days and hosted 66 esports tournaments. But the more significant shift has been in ambition. Dubai's model has always been pragmatic: build the infrastructure, attract the companies, and let the ecosystem follow.

Supporting local developers

The DMCC free zone - 100% foreign-owned, with zero personal income tax and home to more than 150 games companies - has made the UAE one of the most accessible entry points in the region for established international studios. What that model had not produced, until recently, was a serious push towards homegrown IP.

That is beginning to change. In March 2026, the Dubai Department of Economy and Tourism and Dubai Culture launched GameForward, an accelerator targeting Emirati developers with support in game design, monetisation and publishing. Finalist teams will also pitch for grant funding at DEF.

A multi-year partnership between Xsolla and the Dubai Films and Games Commission is also designed to give Dubai-based developers a commercial pathway to international markets - something the city's games commissioner said the market had previously lacked. This is also part of the Emirate's plan to become "The startup capital of the world."

From attracting studios to creating them

The Dubai Gaming Retreat, organised by the Dubai Media Council and attended by Crown Prince Sheikh Hamdan bin Mohammed bin Rashid Al Maktoum alongside representatives of 80 leading local and international gaming companies, set the political tone.

The five strategic priorities discussed at the retreat include talent, governance and regulation, funding, marketing and infrastructure, suggesting Dubai understands what it still needs to build, not just what it has already assembled.

The harder question is whether Dubai will eventually produce globally successful homegrown studios, rather than simply being the city where international studios choose to set up.

Morocco: the most ambitious latecomer

Morocco's entry into this conversation is recent but forceful. The third Morocco Gaming Expo drew a record 80,000 visitors to Rabat and produced a series of concrete announcements. Pixoul Gaming confirmed plans to open a Casablanca subsidiary by 2027, while GameEarly will establish a regional hub in Rabat by late 2026.

Local developer Ivalice Studio, founded in Rabat in 2025, also unveiled its debut title, Rogue Fantasy: Ever-Shifting Worlds. Morocco will make its Gamescom debut in Cologne this August with a 102m² national pavilion.

Morocco, which ranks among Africa's five largest games markets but sits behind the continent's leading trio of Egypt, Nigeria and South Africa, is targeting $3bn in games revenue and 10,000 direct jobs as part of its 2030 plan, with the Rabat Gaming City project serving as the centrepiece of that strategy.

Minister of youth, culture and communication Mohamed Mehdi Bensaid has framed the ambition clearly: Morocco wants to move from consuming games to creating and exporting them.

International support is also growing. The EU signed a strategic agreement with Morocco on the sidelines of MGE, building on the €10m ($11.3m) Support Programme for Cultural and Creative Industries launched in 2023.

The partnership focuses on three priorities: strengthening university and vocational training for game development, conducting market studies to identify opportunities and challenges for Moroccan studios, and creating stronger links between Moroccan and European gaming ecosystems through business missions and professional exchanges.

The next challenge

Nevertheless, Morocco is starting from a lower base than Saudi Arabia and still faces skills shortages, limited access to risk capital and a gap between studio activity and commercial success.

Its immediate competitive advantage may lie in its established offshoring industry, which employed 148,500 people by the end of 2024. Gaming fits naturally within that services-export model.

The challenge is that providing development services for international publishers and building valuable original IP are fundamentally different businesses. Whether Morocco reaches its $3bn ambition will depend on how successfully it transitions from one to the other.

Egypt: a market without a strategy

Egypt is the largest games market by player base among the MENA-3 markets, yet it is the only country in this list without a dedicated national strategy.

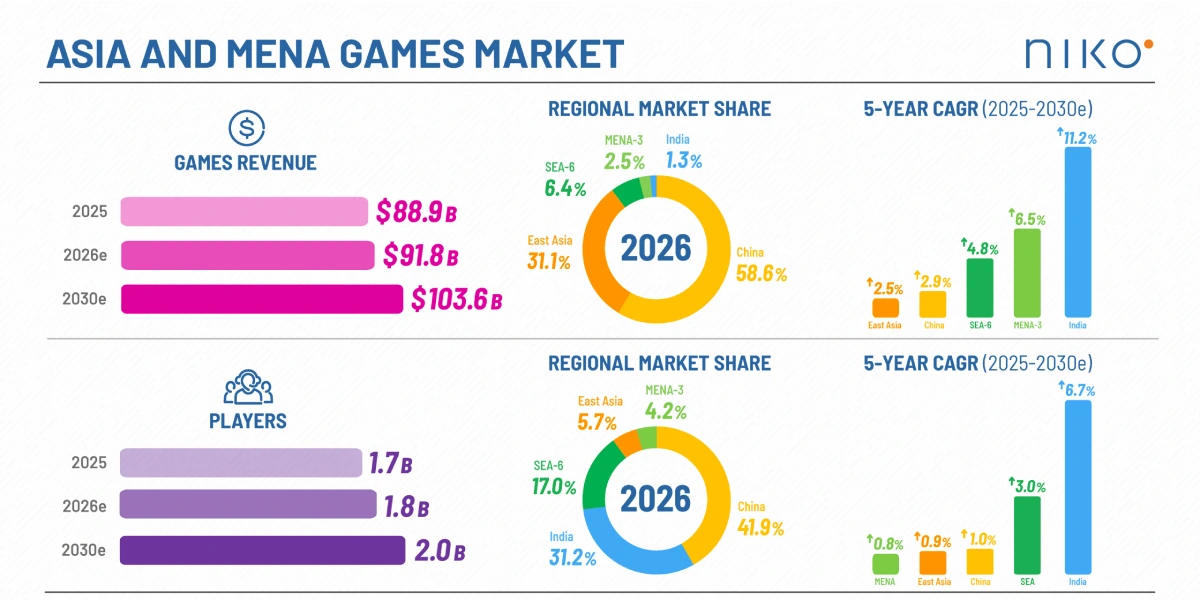

According to Niko Partners, the combined games market across Saudi Arabia, the UAE and Egypt is projected to reach $3bn in player spending by 2030, making it the world's second fastest-growing games market by revenue after India.

Egypt currently accounts for 7.2% of that combined MENA-3 revenue, which clearly is not due to a shortage of players but to weaker monetisation infrastructure and the absence of a coordinated policy direction.

More than half of Egypt's population is under 30, smartphone penetration continues to rise, and affordable mobile data has expanded gaming well beyond Cairo and Alexandria into rural areas. The underlying conditions for a major games industry are already in place.

Policy remains the missing piece

What Egypt lacks is a strategy to match those fundamentals. Saudi Arabia has its National Gaming and Esports Strategy, while Morocco has a dedicated, EU-backed gaming roadmap targeting 2030.

Egypt's existing digital initiatives, including its ICT 2030 Strategy and Digital Egypt programme, focus on wider digital transformation rather than gaming specifically. Gaming is also absent from Egypt’s Vision 2030 plan, leaving the country without a sector-specific plan comparable to those of its regional peers.

The National Strategy for Youth and Sports 2025-2032, launched in August 2025, does include plans to establish a dedicated esports federation and organise national esports competitions. However, those measures sit within a broader sports policy rather than a funded, target-driven strategy for the games industry.

Strong foundations, limited support

Egypt's developer community, particularly around Cairo, is well established and continues to grow, with local studios increasingly producing Arabic-language games for regional audiences. The challenge is institutional support.

Unlike Morocco's Rabat Gaming City or Saudi Arabia's network of accelerators and investment programmes, Egypt has yet to build dedicated structures that help studios scale. As a result, many Egyptian developers continue to grow largely through their own efforts despite operating in the region's biggest gaming market.

Beyond 2030

Saudi's vision is backed by sovereign wealth capital, deployed institutional infrastructure, and a government willing to write very large cheques - though even Riyadh is not insulated from the industry's structural pressures.

Morocco is backed by ministerial energy, EU partnership and an emerging studio scene, but the revenue base is thin and the talent pipeline is early.

The UAE is backed by a world-class business environment that attracts foreign companies and is now, with GameForward and the Dubai Gaming Retreat, beginning to ask harder questions about homegrown IP on a timeline that runs to 2033.

Egypt's potential is structural - demographics, market size, developer talent - but the strategic wrapper is absent, and potential without policy tends to dissipate.

Every country listed has a vision for where it wants to be by 2030. Whether any of them build a games industry that endures beyond that deadline is a different question entirely - and one that will be answered by studios, talent and commercially successful games, not by strategy documents.

Companies