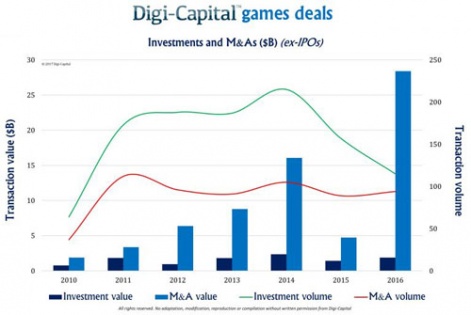

Given the $8.6 billion Tencent-Supercell and $5.9 billion Activision Blizzard-King deals which completed during the last 12 months, it’s little surprise 2016 was a record for mobile game-related mergers and acquisitions (M&A).

2017 may not reach that level in terms of billions of dollars, but it’s already seen some interesting deals, notably:

- the closing of Netmarble’s rumoured $700 - $800 million acquisition of parts of Kabam,

- Take-Two’s $250 million purchase of Social Point, and even

- Zynga’s secretive $42.5 million takeover of Harpan.

So, in the context of a fast-maturing Western market and some fast-expanding Asian companies looking for international reach, who’s next?

Match-making

We may not have a crystal ball but we have attempted to match 10 companies who could be buyers with 10 companies who could be available… at the right price.

Not that we’re saying these deals could happen, merely that these are deals which make sense in some way and which also highlight deeper trends driving sector consolidation.

N.B. The list is organised in increasing estimated deal size.

Click here to view the list »